All Categories

Featured

Table of Contents

The are whole life insurance and universal life insurance policy. expands cash worth at a guaranteed rates of interest and also via non-guaranteed dividends. expands money value at a dealt with or variable rate, depending on the insurance company and plan terms. The cash value is not included in the fatality advantage. Cash money value is a function you make the most of while alive.

The plan financing rate of interest rate is 6%. Going this path, the interest he pays goes back into his plan's money value instead of a financial institution.

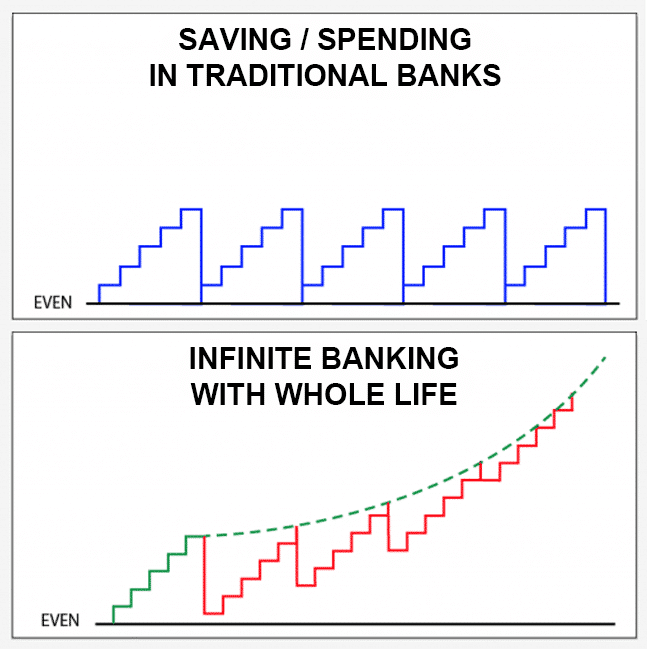

Infinite Bank Concept

The concept of Infinite Banking was created by Nelson Nash in the 1980s. Nash was a finance expert and fan of the Austrian college of business economics, which promotes that the value of products aren't explicitly the result of standard financial frameworks like supply and need. Rather, individuals value cash and products differently based upon their economic status and requirements.

One of the pitfalls of standard financial, according to Nash, was high-interest prices on finances. Long as financial institutions set the interest rates and funding terms, individuals didn't have control over their very own wealth.

Infinite Financial requires you to own your economic future. For ambitious people, it can be the finest economic tool ever before. Here are the benefits of Infinite Financial: Perhaps the single most valuable element of Infinite Financial is that it boosts your capital. You do not need to go through the hoops of a traditional financial institution to get a financing; just demand a policy lending from your life insurance policy firm and funds will certainly be offered to you.

Dividend-paying whole life insurance policy is extremely reduced risk and provides you, the policyholder, a lot of control. The control that Infinite Financial provides can best be organized right into two categories: tax advantages and asset protections - cash value life insurance infinite banking. Among the reasons entire life insurance policy is excellent for Infinite Financial is how it's tired.

Infinite Banking Reviews

When you use entire life insurance policy for Infinite Financial, you get in right into a personal contract in between you and your insurance coverage company. This personal privacy provides certain property protections not found in other monetary automobiles. Although these defenses might vary from state to state, they can include protection from property searches and seizures, protection from reasonings and protection from financial institutions.

Whole life insurance policy policies are non-correlated properties. This is why they work so well as the financial foundation of Infinite Financial. No matter what happens on the market (supply, genuine estate, or otherwise), your insurance coverage plan maintains its worth. A lot of people are missing out on this important volatility buffer that helps safeguard and expand wide range, instead dividing their cash right into 2 buckets: savings account and investments.

Market-based financial investments grow wealth much quicker however are exposed to market changes, making them naturally dangerous. What if there were a 3rd pail that provided security however additionally moderate, guaranteed returns? Whole life insurance is that third container. Not just is the price of return on your entire life insurance plan assured, your death benefit and premiums are additionally guaranteed.

Below are its major benefits: Liquidity and access: Plan lendings offer instant access to funds without the restrictions of typical bank fundings. Tax efficiency: The cash value expands tax-deferred, and policy loans are tax-free, making it a tax-efficient device for building wide range.

Cash Flow Whole Life Insurance

Property security: In several states, the cash money worth of life insurance policy is shielded from lenders, adding an extra layer of financial security. While Infinite Banking has its benefits, it isn't a one-size-fits-all solution, and it features substantial drawbacks. Below's why it may not be the finest approach: Infinite Financial usually requires intricate policy structuring, which can puzzle insurance holders.

Imagine never needing to worry regarding financial institution lendings or high interest rates again. What happens if you could obtain money on your terms and build wealth at the same time? That's the power of boundless financial life insurance coverage. By leveraging the money value of entire life insurance policy IUL plans, you can grow your wide range and obtain cash without counting on traditional banks.

There's no collection funding term, and you have the liberty to choose the repayment timetable, which can be as leisurely as settling the financing at the time of fatality. This versatility reaches the servicing of the lendings, where you can choose interest-only settlements, maintaining the car loan equilibrium flat and workable.

Holding cash in an IUL fixed account being credited passion can often be far better than holding the cash on deposit at a bank.: You've constantly imagined opening your own bakery. You can obtain from your IUL plan to cover the preliminary expenses of leasing a space, acquiring devices, and employing personnel.

Infinite Banking Agents

Individual loans can be acquired from standard financial institutions and credit report unions. Borrowing money on a credit score card is normally very pricey with annual portion rates of rate of interest (APR) often reaching 20% to 30% or more a year.

The tax therapy of policy car loans can vary substantially depending on your nation of home and the certain terms of your IUL policy. In some regions, such as North America, the United Arab Emirates, and Saudi Arabia, policy lendings are normally tax-free, providing a substantial benefit. However, in other territories, there may be tax ramifications to consider, such as potential taxes on the financing.

Term life insurance coverage only supplies a death advantage, with no cash money worth accumulation. This means there's no cash value to obtain versus. This write-up is authored by Carlton Crabbe, Chief Executive Policeman of Capital permanently, a specialist in giving indexed universal life insurance coverage accounts. The details supplied in this post is for educational and informational purposes just and need to not be interpreted as economic or investment recommendations.

For loan police officers, the considerable guidelines enforced by the CFPB can be seen as difficult and limiting. First, lending policemans often argue that the CFPB's guidelines develop unnecessary bureaucracy, leading to more documents and slower lending handling. Guidelines like the TILA-RESPA Integrated Disclosure (TRID) guideline and the Ability-to-Repay (ATR) requirements, while targeted at safeguarding consumers, can lead to delays in shutting deals and enhanced operational prices.

{kind=link}

Latest Posts

Bank On Yourself: Safe Money & Retirement Savings Strategies

Infinite Banking Center

Be Your Own Bank [Top 7 Benefits Of Being Your Own Banker]